Purchasing a home with a low income may seem challenging, but it’s entirely possible with the right strategies and resources. With careful planning, leveraging available programs, and adopting smart financial practices, you can achieve the dream of homeownership. This guide will walk you through the essential steps. As for how much you need might NOT be as much as you think. Here is another article that touches this subject that you might find useful, What To Save For When Buying A Home.

1. Evaluate Your Financial Situation

Before beginning your home-buying journey, take a close look at your finances:

- Check your credit score: A good credit score increases your chances of mortgage approval and can secure lower interest rates. Aim for a score of 620 or higher, but note that FHA loans can accommodate scores as low as 500.

- Create a budget: Calculate your monthly income, expenses, and how much you can afford for housing costs.

2. The Importance of Speaking with a Realtor® and Lender

Whether you’re ready to buy now or just starting your research, talking to a Realtor® and a lender is a critical first step. Here’s why:

- Building a Plan: A Realtor® and lender can help you map out the home-buying process, set realistic goals, and create a timeline that works for you.

- Exploring Your Options: Lenders can evaluate your financial situation and explain programs you may qualify for, including low down payment loans or assistance programs.

- Understanding the Process: Working with professionals ensures you fully understand each step, from pre-approval to closing.

Even if you’re just gathering information for the future, having a conversation now can set you up for success later.

3. Hard Pull vs. Soft Pull: What’s the Difference?

When discussing your financial situation with a lender, it’s essential to understand the difference between a hard credit pull and a soft credit pull:

- Soft Credit Pull:

- What It Is: A soft pull is a credit inquiry that does not affect your credit score. It provides lenders or service providers with a general overview of your creditworthiness.

- When It’s Used: Often used for pre-approvals or initial evaluations before applying for a mortgage or other financial products.

- Benefits: You can explore your options and see where you stand without worrying about your credit score being impacted.

- Hard Credit Pull:

- What It Is: A hard pull is a more in-depth inquiry into your credit report and can affect your credit score slightly.

- When It’s Used: Typically occurs when you officially apply for a loan, such as a mortgage. Lenders need this to make a final decision.

- Impact: It can lower your credit score by a few points, but the effect is usually temporary.

As your Realtor®, I can connect you with trusted lenders who can perform a soft pull to help you understand your options without impacting your credit score. Once you’re ready to move forward, they’ll guide you through the hard pull and loan application process.

4. Save for a Down Payment

While you’ll need some savings, it might not be as much as you think. Many resources can reduce upfront costs:

- Down Payment Assistance Programs: Grants or low-interest loans can cover part of your down payment.

- Seller Assist: This allows the seller to contribute toward your closing costs, reducing the amount you need to save. As your Realtor®, I can negotiate this for you and explain how it works.

Having some savings is essential, but these options make homeownership more attainable.

5. Explore Low-Income Homebuyer Assistance Programs

Numerous programs are designed to help low-income buyers:

- Federal Housing Administration (FHA) Loans: Require a low down payment (as low as 3.5%) and flexible credit requirements.

- USDA Loans: Offer zero down payment options for eligible rural and suburban properties.

- VA Loans: Available to veterans and active-duty military members with no down payment required.

- State and Local Assistance Programs: Many states provide grants, low-interest loans, or down payment assistance programs for first-time buyers.

6. Find an Affordable Home

Work with a real estate agent experienced in helping low-income buyers:

- Search within your budget: Stick to homes you can comfortably afford.

- Consider fixer-uppers: Homes in need of minor repairs often cost less and may qualify for renovation loans.

- Look beyond major cities: Suburban and rural areas often offer more affordable options.

7. Negotiate Closing Costs

Closing costs can add up, but there are ways to reduce them:

- Ask the seller to contribute: Through seller assist, a portion of your closing costs can be covered.

- Shop for services: Compare rates for title insurance, home inspections, and other services.

- Use lender credits: Some lenders offer credits in exchange for slightly higher interest rates.

8. Take Advantage of Tax Benefits

Homeownership comes with tax advantages that can ease the financial burden:

- Mortgage interest deduction: Deduct the interest paid on your mortgage from your taxable income.

- Property tax deductions: Deduct property taxes paid during the year.

- First-Time Homebuyer Credits: Some states offer tax credits for first-time buyers.

9. Plan for Ongoing Expenses

Owning a home involves ongoing costs:

- Budget for maintenance: Set aside funds for repairs and upkeep.

- Understand property taxes and insurance: These costs are typically included in your mortgage payment.

- Avoid overextending your budget: Resist the temptation to spend the maximum loan amount you’re approved for.

Final Thoughts

Buying a house with a low income is achievable with proper planning, the right support system, and a clear understanding of the process. Whether you’re ready to buy now or just starting your research, speaking with a Realtor® and a lender is an important first step. Together, we can build a customized plan, explore assistance programs, and discuss strategies like seller assist and down payment grants.

As a dedicated Realtor®, I can guide you through the process, connect you with experienced lenders who offer soft credit pulls, and point you toward resources that make homeownership more accessible. Contact me today, and let’s start your journey toward owning your dream home!

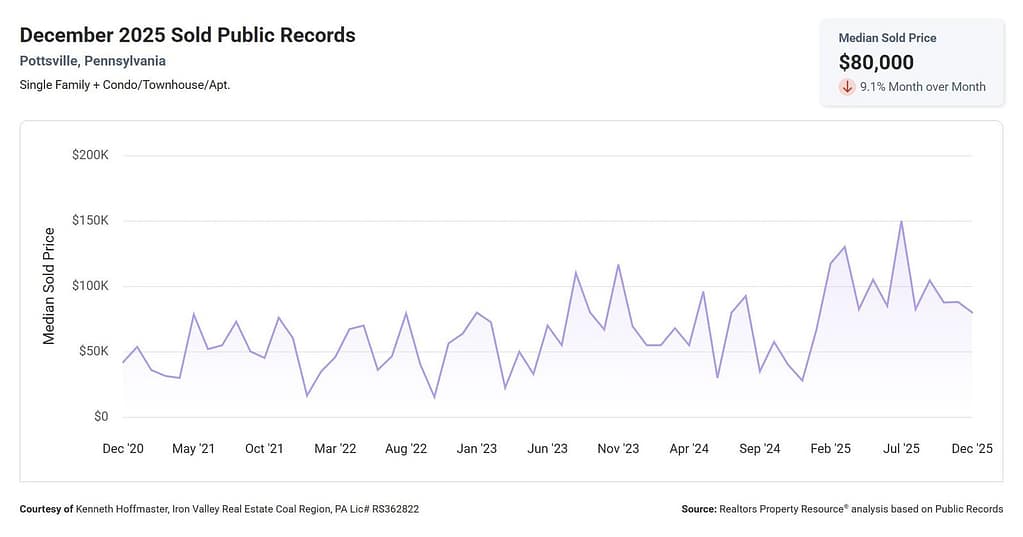

- Pottsville, PA Real Estate Market Update – December 2025: What Buyers & Sellers Need to Know

Pottsville’s real estate market remains seller-leaning as we close out 2025, with low inventory, steady buyer activity, and strong long-term property values. Here’s a clear, data-driven breakdown of what’s happening locally — and what it means if you’re buying or selling in 2026.

Pottsville’s real estate market remains seller-leaning as we close out 2025, with low inventory, steady buyer activity, and strong long-term property values. Here’s a clear, data-driven breakdown of what’s happening locally — and what it means if you’re buying or selling in 2026. - How To Stretch Your Options, Not Your Budget

One of the biggest homebuying advantages you can give yourself… Read more: How To Stretch Your Options, Not Your Budget

One of the biggest homebuying advantages you can give yourself… Read more: How To Stretch Your Options, Not Your Budget - Your Equity Could Change Everything About Your Next MoveA lot of people are asking the same thing right… Read more: Your Equity Could Change Everything About Your Next Move

- Why Selling Your House This Winter Gives You an EdgeSpring gets all the attention, but it’s not always the… Read more: Why Selling Your House This Winter Gives You an Edge

- This May Be the Best Time To Buy a Brand-New HomeNew home construction today is giving buyers something it feels… Read more: This May Be the Best Time To Buy a Brand-New Home

- Why More Homeowners Are Giving Up Their Low Mortgage RateIf you’re like a lot of homeowners, you’ve probably thought:… Read more: Why More Homeowners Are Giving Up Their Low Mortgage Rate

- The 3 Housing Market Questions Coming Up at Every Gathering This SeasonWhether it’s at a family gathering, your company party, or… Read more: The 3 Housing Market Questions Coming Up at Every Gathering This Season

- How To Find the Best Deal Possible on a Home Right NowWant to know how to find the best deal possible… Read more: How To Find the Best Deal Possible on a Home Right Now

- Why So Many People Are Thankful They Bought a Home This YearHomebuyers are weighing their options right now, and they certainly… Read more: Why So Many People Are Thankful They Bought a Home This Year